Throughout much of the third quarter global equities declined in unison with one exception: U.S Stocks. For the week of October 10, US equities joined in to show losses across virtually every sector. Through October 15, European stocks were down down 4.9% for the year. Japan had lost .6%, with China and the broader emerging markets index down 20% and 14.4% respectively. After last week’s losses, US stocks held on to gains of 4% (1).

The US Downturn refers to negative performance during the week of October 10, 2018.

This has created a divergence in the perspectives of US investors, who have a sense that all is well in financial assets, and foreign investors, who in some cases are seeing their countries’ stocks participating in bear markets. In addition, large cap gains conceal the fact that even many US stocks are faring poorly. As of Wednesday the 10th, the day that the Dow declined 3.2%, 2/3 of the stocks in the S&P 500 Index were participating in a correction or a bear market. (2)

So, which stocks have been doing well this year? Until recently, the stock leadership in the US consisted of only a few stocks. In fact, in July, 98% of the YTD gains in the S&P 500 Index were from just 6 stocks. (3) So what is perceived by our investors as a strong market is merely the result of gains in Amazon, Netflix, Microsoft, and a few other big names.

In July, just six stock made up 98% of YTD gains of the S&P 500 index

Toews Strategies turn Defensive in October

Throughout much of the 3rd quarter, Toews strategies held International Stock Exposure in a defensive posture but held a bullish posture with US Stocks and High Yield bonds. During the first and second weeks of October, we moved to a fully defensive posture across all asset classes as markets deteriorated. Our signals have indicated that a downward trend had begun. However, there’s no way of knowing whether the direction of the market will reverse or pick up negative momentum in the fourth quarter. The positive for stocks is that earnings continue to be strong. The negatives include rising rates, trade frictions, and a deteriorating global stock market.

Another factor creating market risks is the possibility that liquidity issues will exacerbate declines. As Pascal Blanqué said in The Economic and Financial Order, “The paradox of liquidity is that it disappears as soon as one is in serious need of it.” As bonds continue to decline, the question remains whether market participants will create a massive one-sided trade that causes losses to accelerate. As we saw last week, bond market losses and rising yields can translate quickly into equity losses. Risk parity programs, hedging strategies, and algorithm trading all may contribute to negative momentum when markets turn lower. Combine all of this with the fact that equity markets are high, and it is easy to understand how stock losses can quickly accelerate.

Toews strategies attempt to address the possibility of either slowly deteriorating or rapidly falling markets in two ways. First, we designed our algorithms to attempt to interpret the initial stages of declines and to exit early, before negative momentum builds. There is a key distinction between this methodology and systems that hedge against losses incrementally as markets move lower. These incremental strategies, in our opinion, may include buy-low, sell-high strategies. A crucial flaw is that they may not address the possibility of rapidly deteriorating markets like October 19, 1987, or losses that could occur in a liquidity crisis. The key is to exit early, before major losses occur.

A second way that Toews strategies address the possibility of losses is with put options that we hold in some of our portfolios that attempt to lessen losses from sudden events. Last week, as markets turned lower, we held only partial exposure to equities. In addition, we saw some appreciation in the put options contracts that we held. If the losses had continued to accelerate, those options would have played an increased role in helping to offset declines.

Don’t Preach, Teach

Six years ago, when my sales director, Eben Burr, and I were holding an investor behavioral workshop for advisors, one advisor recounted his experience during the financial crisis. As stocks moved lower and entered free-fall in September and October of 2008, this advisor’s clients pervasively called into his office to ask when he would rebalance the portfolio and buy more stocks to take advantage of the bargain prices.

That story helped anchor our perspective for preparing investors for behavioral challenges. Telling investors about the right course of action isn’t enough. We need our clients to arrive at our meetings telling us what the right course of action is!

In Daniel Coyle’s excellent book, The Talent Code, he articulates processes for building expertise in a field. He introduces us to a substance called myelin. According to Coyle, “Myelin is the insulation that wraps our nerve fibers and increases signal strength, speed, and accuracy. The more we fire a particular circuit, the more myelin optimizes that circuit, and the stronger, faster, and more fluent our movements and thoughts become.” (4)

Take a tennis pro, as an example. At first, anyone who picks up a racket is likely to have a difficult time with their back hand. Over time, as players practice, they build myelin around the complex neural connections involved in executing this skill. Once a player has become an expert, these thoughts and movements become virtually automatic or reflexive for players.

Our clients aren’t irrational. They just haven’t built up myelin to help them make the counter-intuitive decisions that lead to successful investing. We have a three-step process for may help to change that paradigm:

1. Make sure that each client truly understands the concepts that you’re conveying.

How did you learn in school? Was it when the teacher said something in front of the class, or when you were required to know it for a test? Exactly. Interactions with investors should be inquisitive rather than instructive. Examples include: “What is the best time to buy stocks?” “If a manager trails in one three-year period, what do you expect it to do in the following period?” “If markets move sideways for 5 years, what do you think history suggests will happen next?” Provide your clients with a road map that documents each course of action that you plan to take. An example of this type of document is our Investors Owner’s Manual.

2. Repeat it

Or rather, ask your investors to repeat it. This is like practice for your investors. For each counter-intuitive decision that you expect your investors to make, they need to have thought through the course of action that they’ll take multiple times. By the time that the big event occurs, like a stock market crash, ideally their response will be reflexive, just like the tennis pro’s backhand.

3. Help Clients feel it

Decisions about our finances are both intellectual and emotional. Infuse training for investors with emotional cues that will help challenging financial events seem familiar when they occur. Some advisors use language like “life boat drills,” conveying a sense of urgency and importance to financial decisions.

Sketch the scene for your investors: “Several big banks have gone bankrupt, the financial news suggests that the markets are in a state of panic, and stocks have lost 50% in the past 6 months. Now, what do you think the best course of action in this market is?”

Deep practice is the crucial difference between feeling good that you’ve explained something to your clients, and having your investors understand and act in ways that position them against the momentum of the crowd.

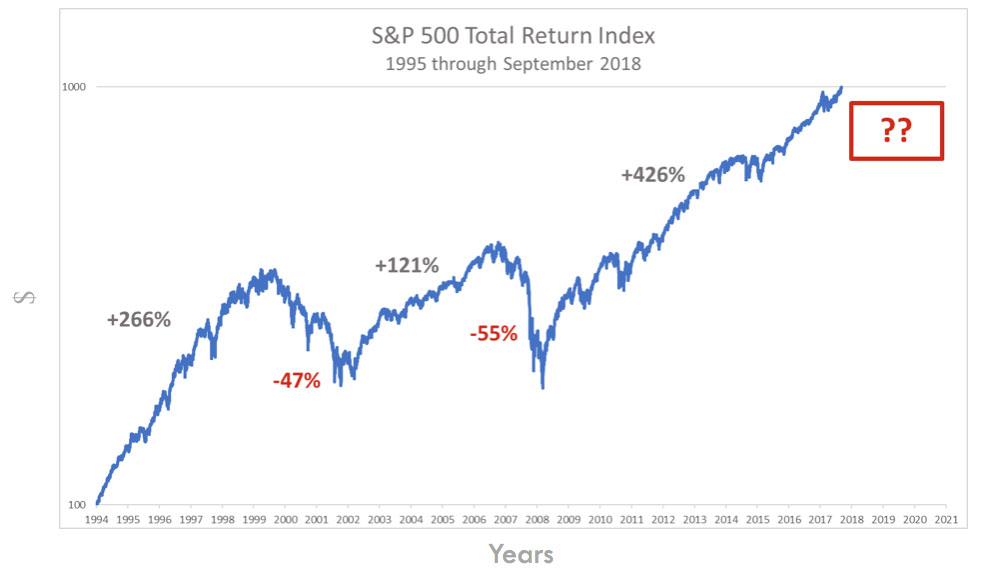

The question du jour for investors: “If stocks have moved higher for almost ten years in one of the biggest bull markets in history, what do you think will happen over the next three years?”

What is the next Trend?

This illustration assumes an initial investment of $100 for ease of calculation. (5)

Disclosure

Prior performance is no guarantee of future results. There can be no assurance, and individuals should not assume, that future performance of any of the portfolios referenced will be comparable to past performance. There can be no assurance that Toews will achieve its performance objectives.

This commentary may include forward-looking statements. All statements other than statements of historical fact are forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” and “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those discussed in such forward-looking statements.

This commentary is intended to provide general information only and should not be construed as an offer of specifically-tailored individualized advice. Please contact your investment adviser, accountant, and/or attorney for advice appropriate to your specific situation.

This document refers to the performance of the majority of Toews portfolios to illustrate the effect of Toews management on US and intl. stocks and high yield bonds. Performance of individual accounts varied based on the client’s investment risk profile and their specific investment funds. For your individual account performance, please refer to the enclosed quarterly statement or the quarterly statement recently sent to you. In addition, not all model portfolios were referenced in this letter. It is not, nor is it intended to be, a comprehensive accounting of Toews asset management. There are other portfolios that Toews manages that performed differently than what is referenced in this letter. For a complete list of GIPS firm composites, their performance results and their descriptions, as well as additional information regarding policies for calculating and reporting returns, please go to www.toewscorp.com. Toews Corporation acts as the investment advisor that implements the asset allocation and models for each of the portfolios. Investors cannot invest directly in an index.

1. Nikkei 225 – https://www.bloomberg.com/quote/NKY:IND Date accessed 10/15/2018; MSCI Emerging Markets Index – https://www.msci.com/end-of-day-data-search – date accessed 10-16-2018; Shanghai Stock Exchange Composite Index https://www.bloomberg.com/quote/SHCOMP:IND date accessed 10-15-2018; Stoxx Europe 600 https://www.stoxx.com/index-details?symbol=SXXP date accessed 10/15/2018; Wilshire 5000 Index https://www.bloomberg.com/quote/WFIVX:US date accessed 10-15-2018

2. https://www.cnbc.com/2018/10/10/more-than-half-of-the-sp-500-is-already-in-a-correction.html date accessed 10-16-2018

3. Source: CNBC https://www.cnbc.com/2018/07/10/amazon-netflix-and-microsoft-hold-most-of-the-markets-gain-in-2018.html Date accessed 10-15-2018 Data as of July 10, 2018

4. Coyle, Daniel. 2009. The Talent Code: Greatness Isn’t Born. It’s Grown. Here’s How. (p. 32). Random House Publishing Group.

5. Source: S&P https://us.spindices.com/indices/equity/sp-500