Ask yourself this question: How do I feel about the stock market (or high yield bond market)? Do I feel 1) optimistic and comfortable, 2) anxious and guarded, or 3) pessimistic and fearful?

The response that most give to this question varies based on what is happening or has just happened in the economy and the financial markets. Optimism and fear are vital emotions that have been a key part of our evolution, but we are tricked by how the markets work. Market optimism peaks after long bull markets, which have historically been the riskiest times to invest. On the other hand, we are fearful about markets after steep declines, which have historically been the best times to invest. In fact, investors wishing to capitalize on their perceptions or emotions may improve their results if they do the opposite of what their intuition suggests. What can be done to improve our outcomes and overcome investor biases?

Solution: Automated Decision Making

When I updated my car lease to a 2017 model, I found several safety features that are, for a safety fanatic like me, awesome. First, if I inadvertently veer over the yellow line, the car automatically steers back into the lane. The car “robotically” stops if it approaches an object and determines that a collision is imminent. Perhaps best of all, the car’s cruise control both steers and controls the distance between itself and other cars. Car manufactures made this simple calculation: Drivers make errors that lead to injuries or deaths, so let’s build cars that attempt to correct for these inevitable mistakes.

We recommend similar “default” decision making for investment portfolios in order to attempt to correct for known biases about financial markets.

Building in Portfolio Defaults

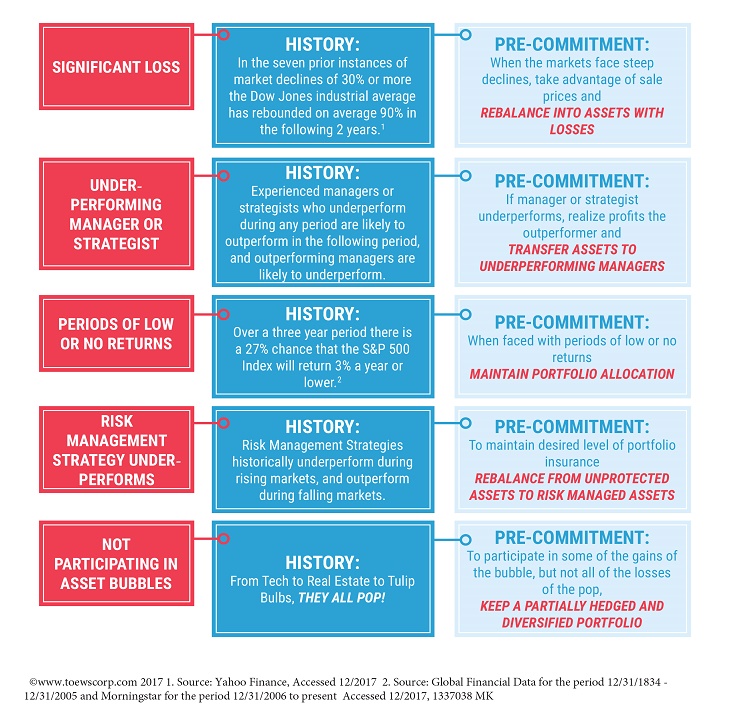

Once fear and regret set in, it’s often too late to reverse biases. We recommend the following two-step process in advance of investor challenges:

- Make sure that your portfolio matches your ability to tolerate risk through all types of markets. We suggest looking back at the worst market environments and examining how your portfolio would have fared. Can you accept a 10%, 20%, 30%, 40%, or 50% loss? Knowing this tolerance in advance of any actual decline is crucial so that, if and when a loss is realized, it is not a surprise.

- Decide in advance of market challenges what action you will take and, to the extent possible, attempt to automate this decision through your investment professional. We’ve compiled a list of challenging market conditions and the most desirable actions (we refer to them here as pre-commitments) that we refer to as an investor “Cheat Sheet” (see next page). For example, when markets experience steep losses, our recommended action is to rebalance the portfolio back to its target allocation. This will add more money to those assets with the steepest losses, potentially positioning the portfolio to prosper during a likely rebound. Notably, this is the opposite of what the crowd does. The crowd tends to exit the investments that have the steepest losses.

What was your response to our initial question? If you feel optimistic and comfortable about markets, it may mean that the markets have recently experienced large gains and that they may be due for a downturn either soon or in the coming year. According to our guide, now is the time to make sure that you have adequate risk management strategies as cushion against market declines and, if you have these strategies in your portfolio, rebalance back to targets to make sure that you are positioned for potential losses ahead.

Markets Continue to Advance in 3Q

Markets continued ahead in the third quarter, gaining 4.5%3. For the year, stocks have risen by double digits ahead of the usually profitable fourth quarter. Our models were fully invested through the quarter with the exception of a partial trade out of the markets for a few days for US equities and a two-week period out of the market for high yield bonds4. Therefore, our models have effectively been fully allocated during 20175. As a result, we’ve been able to produce market-like returns this year and are hopeful that gains will continue as long as possible before the next market fall.

Disclosure

Prior performance is no guarantee of future results. There can be no assurance, and individuals should not assume, that future performance of any of the portfolios referenced will be comparable to past performance. There can be no assurance that Toews will achieve its performance objectives.

This commentary may include forward-looking statements. All statements other than statements of historical fact are forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” and “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those discussed in such forward-looking statements.

This commentary is intended to provide general information only and should not be construed as an offer of specifically-tailored individualized advice. Please contact your investment adviser, accountant, and/or attorney for advice appropriate to your specific situation. This document refers to the performance of the majority of Toews portfolios to illustrate the effect of Toews management on US and intl. stocks and high yield bonds. Performance of individual accounts varied based on the client’s investment risk profile and their specific investment funds. For your individual account performance, please refer to the enclosed quarterly statement or the quarterly statement recently sent to you. In addition, not all model portfolios were referenced in this letter. It is not, nor is it intended to be, a comprehensive accounting of Toews asset management. There are other portfolios that Toews manages that performed differently than what is referenced in this letter. For a complete list of GIPS firm composites, their performance results and their descriptions, as well as additional information regarding policies for calculating and reporting returns, please go to www.toewscorp.com. Toews Corporation acts as the investment advisor that implements the asset allocation and models for each of the portfolios. Investors cannot invest directly in an index.

Pre-commitments serve only as suggested investor response plans and are non-binding.

For additional information about Toews, including fees and services, send for our disclosure statement as set forth on Form ADV by contacting Toews at Toews Corporation, 1750 Zion Road, Suite 201, Northfield, NJ 08225-1844 or (877) 863-9726.

(1) Source: Yahoo! Finance as-of 12/2015. Accessed 12/2015 The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the Nasdaq.

(2) Source: Yearly closing returns from GFD for the period 12/31/1834 to 12/31/2005 and Morningstar for the period 12/31/2006 to present. The S&P 500 Index is one of the common benchmarks for the U.S. stock market.

(3) Source: Morningstar Direct. S&P 500 Index return for the period 7/1/2017 to 9/30/2017.

(4) Only our Toews All-Equity, Growth, Balanced Growth, Balanced, Balanced Income, Capital Preservation, Defensive Alpha portfolios, TDFI portfolios are referred to as “our models.” We have other portfolios on our platform that did not trade as described herein.

(5) The HY portion of our models was in a defensive position during the periods 3/9/2017 to 3/30/2017 and 8/11/2017 to 8/30/2017. The US stock portion of our models was 2/3rds invested during the period 7/6/2017 to 7/13/2017. The remaining portions of our models have been fully invested during 2017.